Every healthcare provider knows how crucial good malpractice coverage is when it comes to making sure you are covered in the event that a claim is filed. That’s why it’s essential to make sure you proactively ask the right questions about malpractice insurance for locum tenens assignments.

Not all insurance policies are created equal––and the kind of coverage you have, or the insurance company you are with, can make a huge difference in the event that a claim is filed against you.

When it comes to medical malpractice insurance it’s important to understand how coverage works so you can make the best and most informed decisions about which locum agencies you partner with, and which assignments you take.

Here are 5 questions to ask about locum tenens malpractice policies:

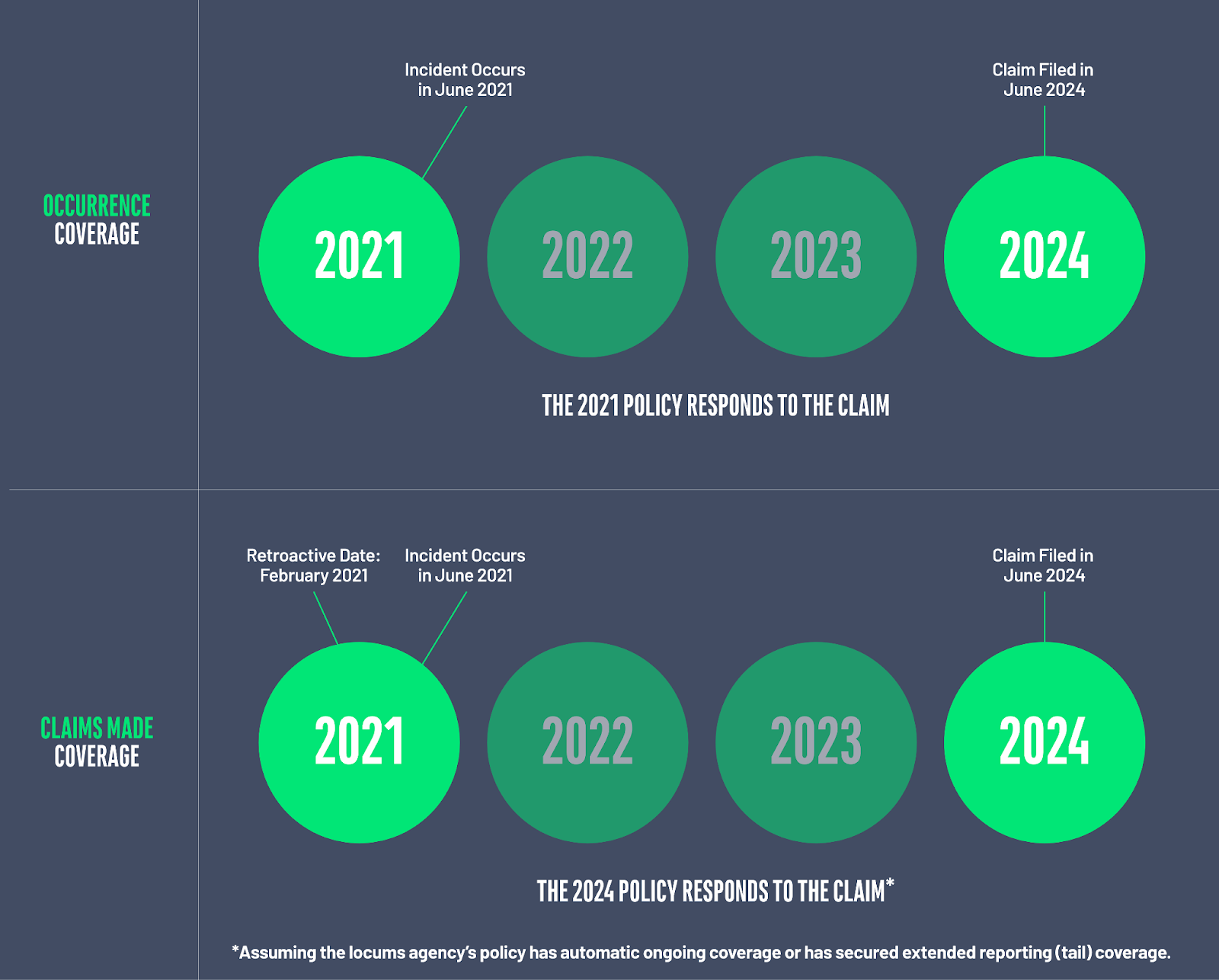

- What type of medical malpractice insurance does your locum agency offer: occurrence-based, or claims-made-based?

When considering whether to work with a certain locum agency, it is critical to ensure that they provide ongoing coverage for claims that may arise, even if the claim is made after your assignment has ended.

While many locum tenens companies don’t use traditional extended reporting or “tail” coverage; oftentimes, the policy is structured to automatically provide ongoing coverage, even after your assignment has ended. Make sure to look for companies that offer occurrence-based policies, or who contractually agree to provide ongoing coverage after your assignment ends.

- Occurrence-based policies protect against incidents that occur during the policy period, regardless of when a claim is made––which means that extended reporting coverage isn’t necessary after your coverage ends.

- Claims-made policies protect against incidents that arise from services rendered after the retroactive date, but before the policy expiration date––that means if a claim is made outside the policy period, you may not be covered if your agency hasn’t structured ongoing coverage appropriately.

- How does your locum tenens malpractice policy cover defense expenses and indemnity payments?

While all malpractice policies respond to defense expenses as well as any indemnity payments that are incurred, a well-crafted malpractice policy should cover the defense expenses in addition to the indemnity limit. This is an important distinction when considering working with a locum tenens company. If defense expenses are not in addition to the indemnity limit, your entire coverage could be eroded solely by defense expenses, leaving you bare should indemnity damages be awarded to the plaintiff.

- Defense Expenses: refers to the cost of legal defense to respond to any allegations that may be made against you.

- Indemnity Payments: the damages that may be owed as a result of any claims filed against you, whether in the form of a judgment or settlement.

- What insurance company is your locum tenens malpractice coverage policy offered through?

It’s important that your locum tenens agency partners with a reputable and reliable insurance company that will protect you if and when a claim arises. That’s particularly true when it comes to lesser-considered aspects like:

- Financial Strength: Insurance carriers receive financial strength ratings from various rating agencies; we recommend insurance carriers with an A.M. Best rating of at least an A.

- Claims Handling: Some insurance carriers outsource claims handling, while others may not have the internal resources to effectively manage your claim.

At Hayes Locums, we only partner with insurance carriers with an A-rating or better, who are time-tested, and have proven to be strong advocates.

- What happens to my locum tenens malpractice coverage once my assignment is completed?

Make sure you have a clear understanding of what type of insurance a locum tenens company offers, and whether it will cover coverage even after an assignment is over, or if you have ended your relationship with the company.

If Hayes Locums is providing your malpractice insurance, you are covered for claims that arise from assignments that you’ve taken with us, regardless of when a claim is made. Whether you’ve taken a full-time job, or are enjoying retirement, you can rest easy in the confidence that you have malpractice coverage for assignments that you worked through Hayes Locums.

- What happens if a claim is made against me? Will the company support me?

At Hayes Locums, our Risk Management team not only reports claims on your behalf, we’re also engaged with the insurance company and defense counsel throughout the claim process, so you’ll feel supported in the event that a claim arises.